New in Google: Shopping Ads for CSS partners – Everything you need to know

A big change in Google’s Shopping Ads auction: CSSs are now able to drive traffic to their own Product Detail Pages (PDPs) via Shopping Ads. So from now on CSSs will participate and compete in the ad auction like any other merchant. All this in order for Google to be compliant with Article 6(5) of the European DMA, which has become active by March 6, 2024. This blog post article explains everything there is to know and what we expect from these changes.

What’s new?

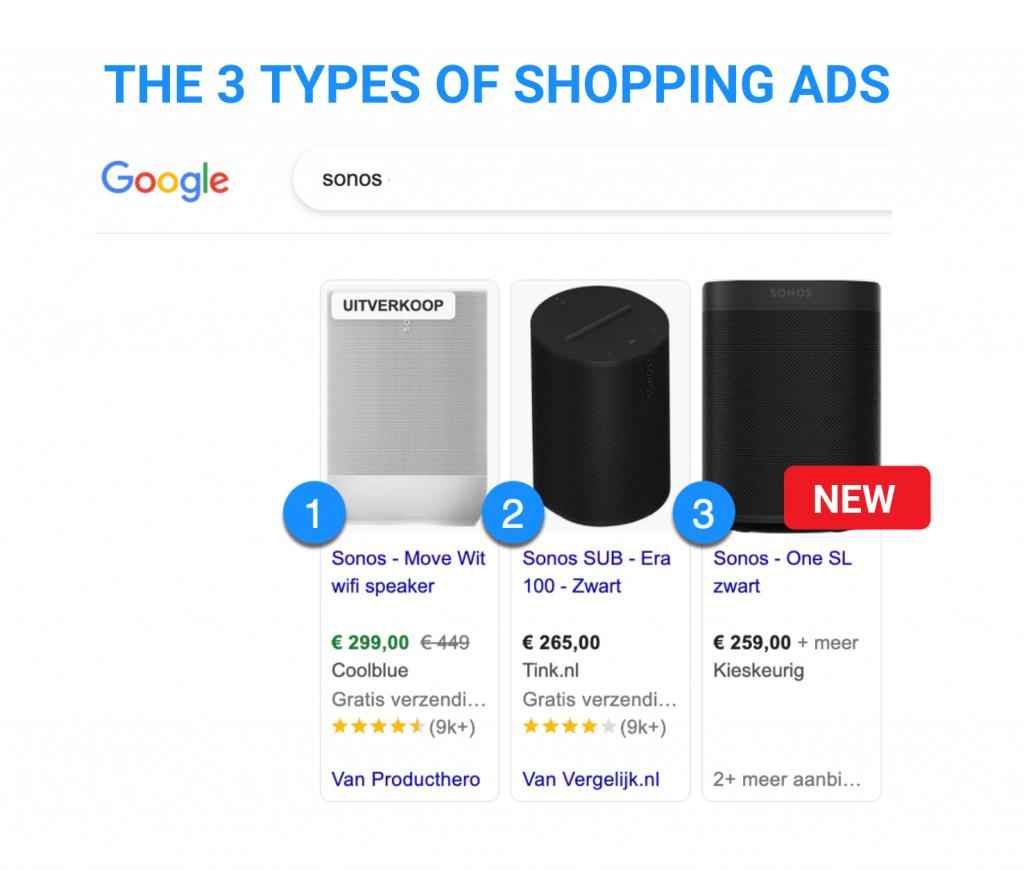

We Googled “Sonos” and spotted the 3 different types of shopping ads on the search engine result page (SERP). Numbers 1 and 2 have existed since 2018, and number 3 is new since 2024:

- Merchant advertises for its own product page – the Google Ads account and campaigns are owned and managed by the merchant. The merchant uses Producthero CSS for financial benefits, support benefits, and additional control and insights. Advertising via a CSS partner has been possible since 2018.

- CSS advertises for the merchant’s product page – the Google Ads account and campaigns are owned and managed by the CSS. The merchant pays the CSS for ad clicks (CPC) or transactions (affiliate commission / CPA). It is possible for CSS partners to advertise on behalf of merchants since 2018.

- NEW: CSS advertises for their product pages – the Google Ads account and campaigns are owned and managed by the CSS. The consumer goes to the CSS website where merchants and prices are compared. The CSS monetizes the clickouts from its website: clicks (CPC) or transactions (affiliate commission / CPA). This is the new ad format: It has become possible for CSSs to advertise for their own website since 2024.

What is the background of the DMA?

The Digital Markets Act (DMA) is EU regulation to maintain contestable digital markets and promote fair commercial practices.

Google is considered a gatekeeper: market operators which provides “core platform services” (“CPS”) with significant impact, is an important gateway and has an entrenched and durable position.

As a gatekeeper, Google is not allowed to preferentially rank its own product or service offerings, or those of a business user it controls, on its CPS (Article 6(5)). The gatekeepers were required to comply with the DMA by March 6, 2024.

What is the background of Google’s CSS Partner Program?

In 2017, the European Commission judged that by placing Product Listing Ads on the Search Engine Result Page (SERP), Google favoured Google Shopping – its own Comparison Shopping Service (CSS).

Therefore in 2018, Google introduced the CSS Partner Program, in which competing Comparison Shopping Services also got access to place ads in this product ad box on the SERP. Therefore the CSS partner program enabled competing CSSs to advertise products the same way Google Shopping (Google’s own Comparison Shopping Service) can.

This meant that CSSs were given the opportunity to advertise products on behalf of merchants. It resulted in merchants having a choice via which CSS(’es) they want to advertise their products on the Google search engine results page (SERP).

Google CSS partners with various business models started to arise. They can be segmented in 3 different categories:

1. Publisher CSSs – the classic comparison websites with CPC or affiliate commission business models

2. Service-led CSSs – fee for campaign management or consultancy services

3. SaaS-led CSSs – like Producthero – provide additional tools and services that empower the merchants’ own campaigns.

Why this new ad format?

The new ad format is a solution for CSSs that want to drive traffic to their own website, instead of directly to merchants.

With the measures Google took with the CSS Partner Program in 2018, competing CSSs have the same access to the PLA box as Google Shopping has. However, the competing CSSs with a publisher model (e.g. Kelkoo, Idealo) still did not see improvement in why they initially started their complaint towards the EU for traffic to their CSS website. Historically these comparison shopping services are highly dependent on traffic coming from Google.

The introduction of Shopping Ads (around 2012) and Google’s ever-evolving organic ranking algorithm have both not been in favor of Comparison Shopping Services. Several have been in business for more than 20 years and saw their traffic drop significantly over the past 10-15 years. Although the measures of the CSS program in 2018 did enable CSS’es to place Product Ads in the same way as Google Shopping did (on behalf of merchants), it did not bring any extra traffic to their own comparison website.

How does the new ad format work?

Just like merchants have a Google Merchant Center, CSS’es have a CSS Center. Here they can upload a product feed, which contains product attributes, from prices and product page URLs, etc.

A CSS can run campaigns for its product pages, just like merchants do for their product pages. They enter the same ad auction as merchants and compete for a position in the same product ad box on Google’s SERP.

What do merchants and agencies think about this?

The several merchants I have talked with are not happy with this development. For many merchants, Shopping Ads are a very important source of revenue. But they find it challenging to have/maintain good visibility of their products in Google, and to make/keep this channel profitable. With lots of merchants in the auction and just a few available ad slots, merchants already experience fierce competition.

With CSS’es entering the auction to promote their price comparison pages, merchants feel that the competition will get more fierce. They expect the volume of their own campaigns to go down, the average CPC to go up and the CPC/affiliate costs of connected comparison shopping channels to go up as well. Is that a valid thought? Yes, I think so. CSS’es are always able to advertise the lowest prices and can create a lot of extra competition in the auction.

What is the expected impact of this change in the Shopping Ads auction?

The expected impact for merchants is that the impression volume of their campaigns will decrease, while the average CPC increases. This is due to the extra competition in the auction. How big the impact is will have to turn out as CSSs are now starting to roll out their campaigns.

If you have your products listed on CPC / Commission based comparison websites that use this campaign type, the volume and cost of these channels might go up as well.

How is this for Comparison Shopping Services (CSS-es)?

This is definitely an opportunity for CSSs with a publisher model (CPC / affiliate commission). They now have an extra option in Google to attract consumers to their comparison website and monetize them.

Although it will be challenging for CSSs with a publisher model too. A CSS has a very different business model than a merchant (CPC or CPA commission after a click from the website), which will definitely limit their maximum bids in the ad auction.

How does Producthero look at this development?

Producthero is an independent CSS platform between the merchant and Google. Because merchants and Google do not pursue mutual goals, we are embraced by more than 10.000 merchants, because they consider us a valuable addition to 1. Google’s support (what they tell you), 2. Google’s ad platform (the control they give you) and 3. Google’s insights (what they show you).

Producthero’s mission is to empower merchants to have a competitive advantage with their campaigns. Running self-managed Shopping campaigns would compete with the campaigns of our customers and it is important for us that our customers can trust us with their data, without any conflicts of interest. Therefore Producthero will remain an independent CSS platform that does not run competing campaigns. Of course, we do follow all the developments with campaign experiments, to keep learning and to keep our customers informed about opportunities and threats.

With these developments, the competition in Google will now get even more fierce, and that’s exactly why everybody can use some Producthero ??